19 April 2024

Self-Assessment Tax Return: Everything You Need to Know

A Self-Assessment Tax Return is a system used by the UK tax authorities (HMRC) to collect income tax from individuals who are not subject to tax through PAYE (Pay As You Earn). It’s essential for anyone earning income that hasn’t been automatically taxed, like freelancers, landlords, and self-employed individuals. Below, we break down everything you need to know about Self-Assessment Tax Returns to help you avoid penalties and ensure you’re fully compliant.

What is a Self-Assessment Tax Return?

A Self-Assessment Tax Return is a form that individuals must fill out and submit annually to HMRC. It allows individuals to report their income, expenses, and other tax-deductible items, so they can calculate how much tax they owe. This applies to self-employed people, freelancers, business owners, and anyone receiving income outside of PAYE.

Who Needs to File a Self-Assessment Tax Return?

If any of the following apply to you, you’ll need to complete a Self-Assessment Tax Return:

- Self-employed individuals

- Individuals with income from renting out property

- Freelancers

- Directors of companies

- Individuals with high incomes

- Those who earn money from foreign income or investments

- Those who receive income from other untaxed sources

If you’re unsure, it’s always a good idea to check with HMRC to confirm whether you’re required to file a return.

Key Dates to Remember for Self-Assessment

Understanding the deadlines for your Self-Assessment Tax Return is crucial to avoid penalties or fines. Here are the important dates:

- October 5: Register for Self-Assessment (if it’s your first time).

- January 31: Submit your online tax return and pay any tax due for the previous tax year.

- July 31: Make a second payment on account for your tax.

Missing these dates can lead to additional charges, so always mark them on your calendar

How to File a Self-Assessment Tax Return

1. Register with HMRC

Before filing your return, you must register with HM Revenue & Customs if you haven’t done so already. This process typically takes a few weeks, so it’s best to do it well ahead of time.

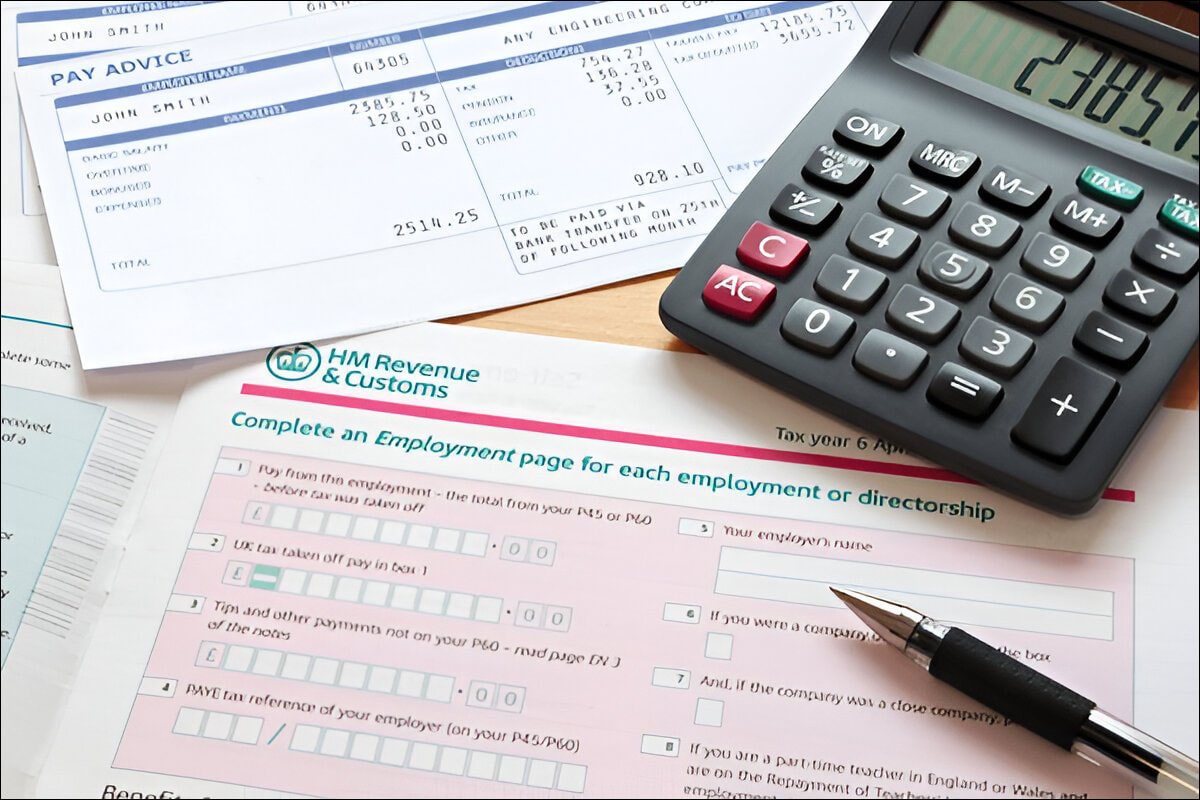

2. Gather Your Documents

To complete your Self-Assessment, you’ll need to have various documents on hand, including:

- Income details (e.g., payslips, invoices, bank statements).

- Business expenses (e.g., receipts, bills).

- P60 and P45 (if applicable).

- Details of other income sources such as rental income, interest, or dividends.

3. Complete Your Tax Return

You can file your Self-Assessment Tax Return online through the HMRC website. It’s user-friendly and guides you through the process. Make sure to double-check your entries and ensure you’re entering accurate information.

4. Pay the Tax You Owe

Once you’ve filed your return, HMRC will calculate how much tax you owe. You’ll need to pay the tax before the January 31 deadline. If you’re unable to pay it in full, you may be able to arrange a payment plan.

How to Avoid Common Self-Assessment Mistakes

While the Self-Assessment process is straightforward, there are common mistakes that can result in penalties. Here’s how to avoid them:

- Be accurate: Double-check all figures to ensure they are correct.

- File on time: Submit your return before the deadline to avoid fines.

- Include all income: Be thorough and report all sources of income, including side jobs and freelance work.

- Claim all allowable expenses: Make sure you take full advantage of any tax deductions you’re entitled to.

- Keep records: Always keep a record of your income, expenses, and any documents you used to complete your return for future reference.

Self-Assessment Penalties and Charges

Failing to file or pay your Self-Assessment tax return on time can result in penalties. Here’s what you can expect:

- Late Filing: A £100 penalty for failing to file your return by the due date.

- Ongoing Late Filing: After 3 months, you’ll incur additional daily penalties of £10.

- Late Payment: Interest charges will be applied to any unpaid taxes.

To avoid these, always file and pay your return promptly.

Common Mistakes to Avoid

1. Missing Deadlines

Missing deadlines is one of the most common mistakes people make when filing their Self-Assessment Tax Return. Keep track of the key dates and ensure you file before the deadline to avoid penalties.

2. Incorrect Reporting of Income and Expenses

Many people fail to report all of their income or overlook certain expenses. Ensure that you provide a complete and accurate report to avoid issues down the line.

3. Failing to Register for Self-Assessment

If you earn income that isn’t subject to tax under PAYE, it’s essential that you register with HMRC as soon as possible. Not registering on time can lead to penalties.

The Importance of Keeping Accurate Records

One of the most important things when managing a Self-Assessment Tax Return is keeping accurate records. This includes invoices, receipts, and bank statements that show your income and expenses. By keeping proper records, you ensure that you report everything correctly and avoid overpaying or underpaying taxes.

Conclusion

Filing a Self-Assessment Tax Return can seem overwhelming, but with the right approach, it can be a straightforward process. By understanding the deadlines, gathering the necessary documents, and filing your return on time, you can ensure that you’re compliant and avoid penalties. If you’re unsure about any aspect of your tax return, don’t hesitate to reach out to HMRC or a tax professional for guidance.

Remember, keeping accurate records throughout the year and staying organized will make the process much easier come tax season.